The Top 40 Industries for SBA Financing in 2020

SBA 7(a) financing is one of the most common ways for small businesses to access capital for growth and business expansion. As highlighted in our recent articles, these loans offer low interest rates and long repayment terms, but navigating the application process can be difficult for many potential borrowers.

In this article, we explore key performance metrics among the most common industries that receive financing through the SBA 7(a) Loan Program. All findings in this article come from an analysis of the top 40industries that have obtained the highest gross number of loan approvals from October 1, 2009, to September 30, 2019 (SBA’s Fiscal Year-End) according to the SBA 7(a) Loan Data Reports on SBA.gov.

Highest-Volume Industries

Over the last decade, more than 545,000 borrowers have benefited from over $200 billion in approved loans through the program. Approximately 50% of the total dollar volume can be attributed to the top 40 industries during this period.

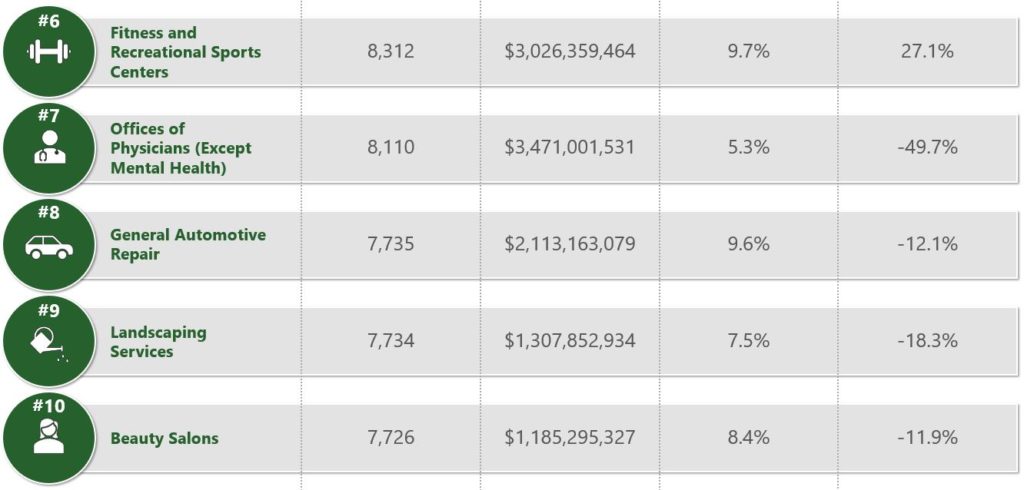

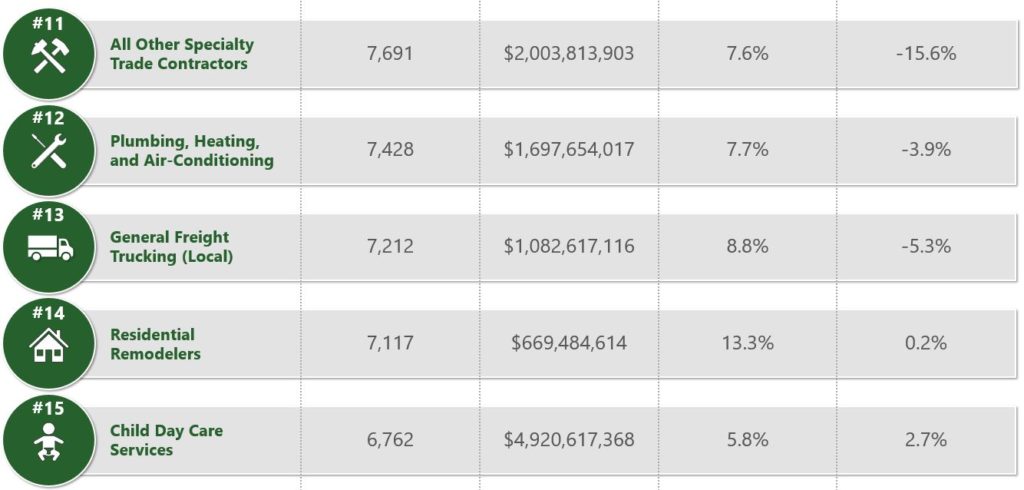

For the top five highest-volume industries, defined as the number of applications submitted and approved, full-service restaurants (28,680), limited-service restaurants (19,141), dentists (10,699), general freight and trucking (8,959) and hotels (8,618) top the list, respectively.

Top Industries for SBA Financing

*Charge-Off Rate FY2010-2019 = # of Charged-Off Loans / (# of Paid-In-Full Loans + # of Charged-Off Loans)

**Growth Rate FY2015 v. FY2019 = (# of Loans FY2019 – # of Loans FY2015) / # of Loans FY2015

Top Performing Industries

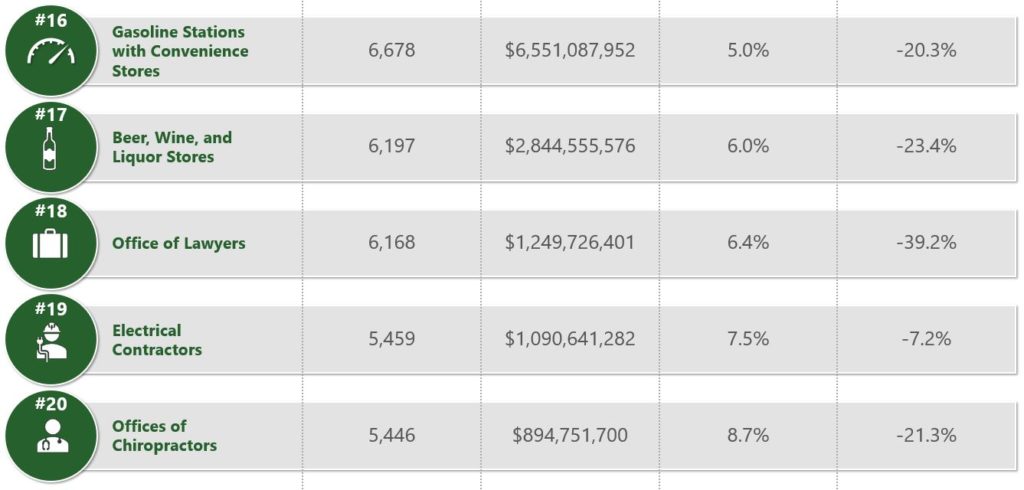

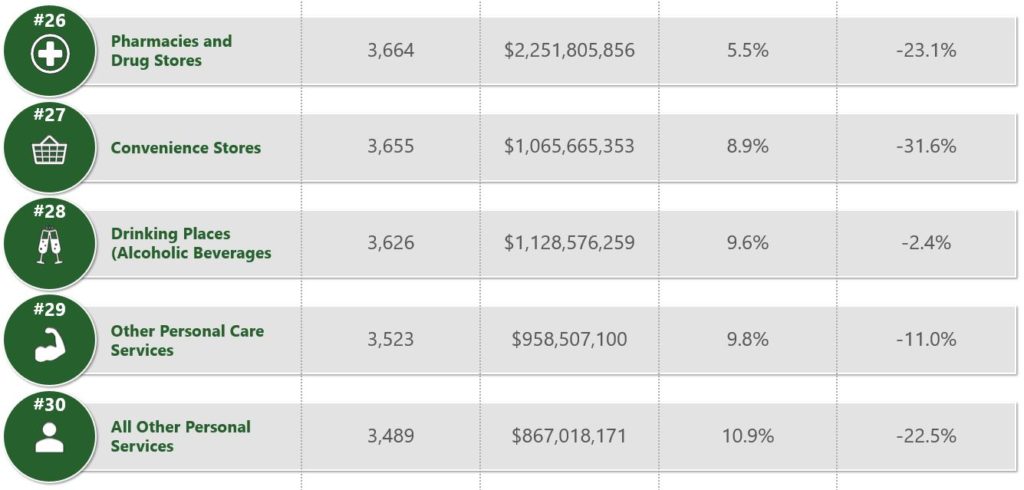

To determine the top performing industries among this group, we evaluated charge-off rate by dividing the total number of loans charged-off by the total number of loans either paid in full or charged-off during the ten-year period. Hotels (2.4%), veterinarians (2.6%), dentists (2.8%), broilers and other meats (4.0%) and insurance agencies (4.6%), ranked as the top five industries with the lowest charge-off rates. Note, this calculation does not include canceled applications that were approved, loans with an outstanding balance or loans that have not yet been recognized as charged-off. To learn more about when a charge-off can officially be justified, see when is a charge-off justified on SBA.gov.

Fastest-Growing Industries

The fastest growing industries among this group were determined by looking at the percentage of growth by number of loans over the past five years (FY2015-2019) across each of the top 40 industries. Snack and non-alcoholic beverage bars grew the fastest, up from 471 approved loans in FY2015 to 610 in FY2019 (29.5% increase). Other industries that experienced growth during this period include fitness and recreational sports centers (27.1% increase), amusement and recreations industries (26.2% increase), insurance agencies (24.9% increase) and child day care services (2.7% increase). Note, the total number of loans approved through the SBA 7(a) Loan Program decreased by 18.2% during this period (63,461 in FY2015 to 51,907 in FY2019).

You can tell from this article that certain industries utilize SBA loans far more than others. Entrepreneurs in these fields may want to seriously consider SBA financing to fuel growth. It’s also important to keep in mind that if your industry did not rank as one of the top industries for SBA financing, small business lending may still be an attractive option, as over 1,200 different industries were approved for an SBA 7(a) loan from FY2010 to FY2019.

To see if SBA financing is the right option for your business, contact Capital Bank at (855) 693-8290 to speak with one of our experts today.

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

Since 2011, Capital Bank has authorized government guaranteed loans for nearly 150 industries.

The Pros and Cons of SBA Loans

If you’re a small-business owner looking for capital to expand, you’ve likely come across SBA 7(a) loans – the nation’s most popular type of loan offered through the U.S. Small Business Administration (SBA).

Let’s look at SBA loans pros and cons to see if a 7(a) loan is right for you.

Perhaps the biggest misconception about these loans is that the SBA lends directly to small businesses. In reality, the SBA 7(a) Loan Program partially guarantees loans made by banks or other direct lenders to eligible small-businesses. The program aims to promote economic growth by encouraging lenders to partner with small businesses that may be struggling to secure financing on reasonable terms. Because of the guaranty, SBA loans tend to have lower monthly payments than other types of loans. However, there are some drawbacks that must be considered prior to starting your application.

To help determine if a 7(a) loan is right for your business, let’s review the pros and cons.

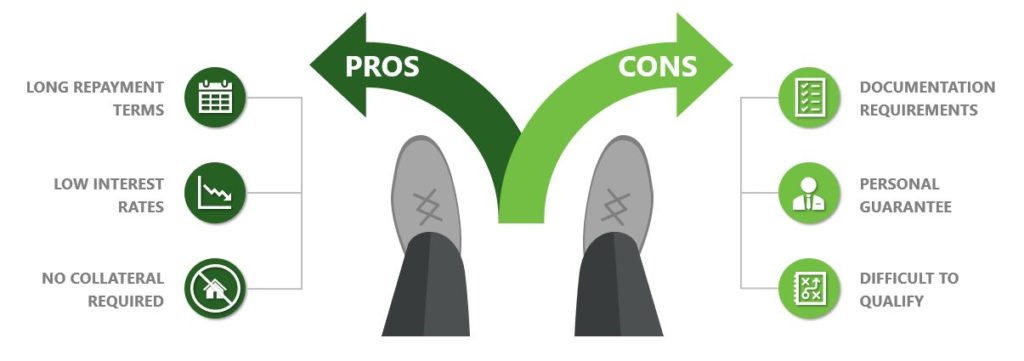

The Pros of SBA Loans

- SBA Loan Pro: Long Repayment Terms

The program offers fully amortizing terms up to 10 years on non-real estate transactions like working capital, equipment or inventory purchases. Longer maturities result in drastically lower monthly payments and conservation of cash flow, creating an opportunity to grow your business faster. In addition, the program allows you to refinance existing debt that may be too expensive.

- SBA Loan Pro: Low Interest Rates

As opposed to online short-term loans which tend to have extremely high rates, the SBA sets maximum interest rates that lenders can charge on 7(a) loans. The maximum interest rate is determined by the size of the loan but typically will not exceed 6.0% (WSJP + 2.75% as of May 18, 2020).

- SBA Loan Pro: No Collateral Requirements

The SBA guaranty helps offset risk, giving financial institutions the flexibility to consider transactions not fully collateralized by business or personal assets. When applying for a traditional bank loan, lenders often require a loan to be fully collateralized by real estate or other tangible assets. Collateral shortfalls are one of the most common reasons credit might not be available elsewhere on reasonable terms, making a small-business eligible to obtain financing through the program.

The Cons of SBA Loans

- SBA Loan Con: Documentation Requirements

The application and funding process can appear to be cumbersome and can take up to several weeks (depending on borrower responsiveness). However, for “small loans” *under $350,000, the SBA prescreens applicants and allows lenders to fast track your application upon meeting certain criteria.

*According to SBA.gov, the number of “small loans” approved through the SBA 7(a) Loan Program in FY2019 represented 72% of all loans approved through the program during this period.

- SBA Loan Con: Personal Guarantee

Lenders will require you to sign a personal guarantee if you own 20% or more equity in the business. If you’re unable to make payments down the road based on the original agreed-upon terms, you’ll need to pay back the lender from your personal accounts or assets.

- SBA Loan Con: Difficult to Qualify

Personal credit and business financials must be solid. The SBA guaranty doesn’t make a bad loan good – it simply makes a good loan stronger and is meant to assist credit-worthy small businesses. While some lenders may only consider 650+ credit scores, others may look at the overall health of your business, including the ability to meet the SBA’s Debt Service Coverage Ratio (DSCR) required minimum of 1.15x.

Although SBA 7(a) loans require investment of time and effort, the overall benefits of the program outweigh the costs for many small-business owners.

If you’re searching for the least expensive and most flexible option, 7(a) loans should be on your radar. While factors like timing and the amount of paperwork matter, extended maturities and lower interest rates tend to have the most profound impact on your business long-term. After taking a look at SBA loans pros and cons, be sure to do your research and consult a preferred lender or lender service provider to ensure you work with a highly qualified partner who optimizes your potential for success.

To see if SBA financing is the right option for your business, contact Capital Bank at (855) 693-8290 to speak with one of our experts today.

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

Spring Storm Questions and Answers

Loans for Engineers: Why SBA Financing Is a Great Resource

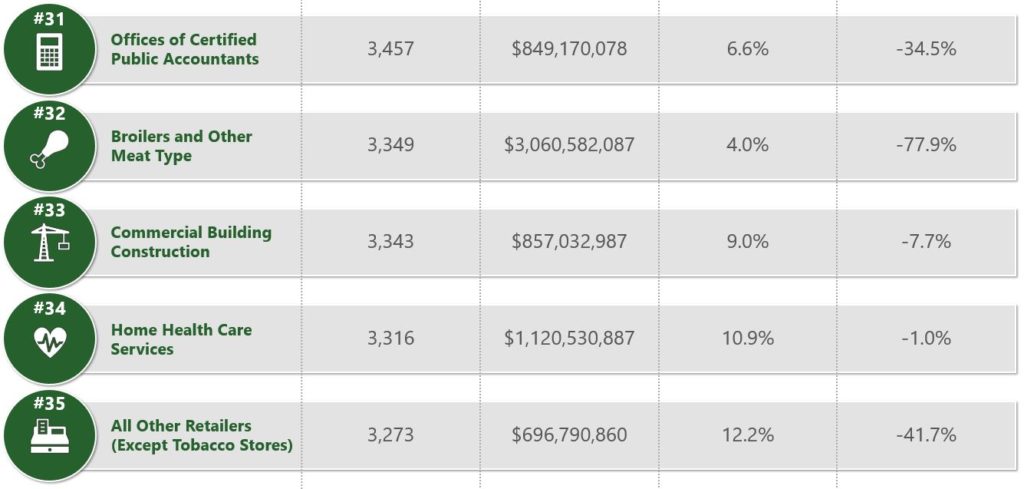

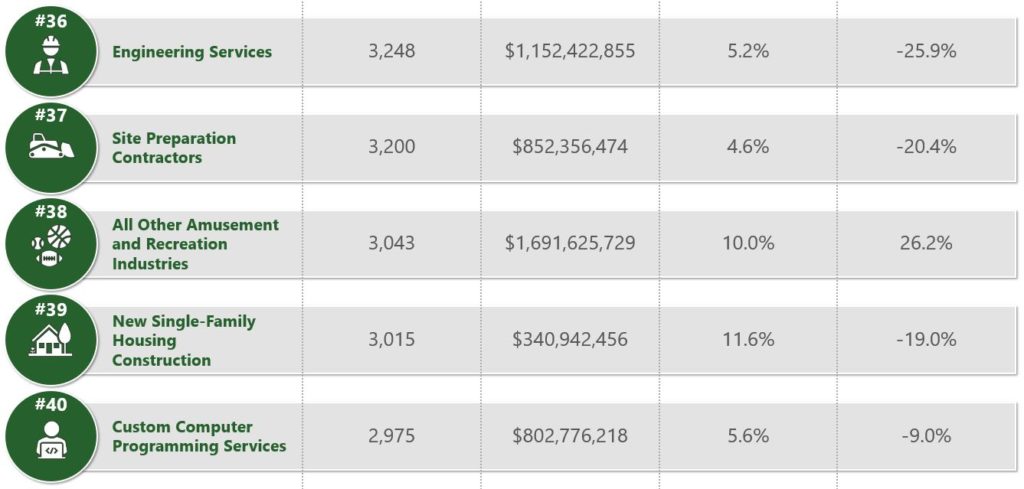

In our latest analysis of the top 40 industries, Engineering Services (NAICS Code: 541330) ranked #20. From October 1, 2009 to September 30, 2019, the number of SBA loans for engineers reached 3,248 totaling roughly $1.15 billion. While “engineering services” is a broad category covering many types of engineers, the need for capital and the value of SBA financing is similar across all engineering categories.

One common misconception is that the SBA lends directly to small businesses. Rather, the SBA 7(a) Loan Program partially guarantees loans made by banks or other direct lenders to eligible small businesses. The program aims to promote economic growth by encouraging lenders to partner with businesses that may be struggling to secure financing on reasonable terms. As a result, SBA loans tend to have low monthly payments, low interest rates and little to no collateral requirements.

According to the U.S. Department of Labor, the employment of industrial engineers is projected to grow by approximately 10% by 2026. With this projected growth, access to capital is a very real need for many engineering firms and it’s critical that engineer entrepreneurs understand common event-driven scenarios and key trends surrounding SBA loans.

Common Ways Engineers Put SBA Loans to Use

Many of the demands listed below are the result of changing practices and technology in the engineering field. While these concepts are vital to growing the industry, many of these scenarios require up-front costs and a potential need for capital.

- Attracting Talent – The demand for highly-skilled, certified employees has dramatically increased since the Great Recession, forcing companies to increase salaries to attract and maintain quality talent.

- Technology – New and more efficient technology continues to emerge. Its usage is not only becoming more popular but necessary for many firms to maintain consistent growth.

- Green Practices – Demand for environmental consideration continues to increase and many firms are paying for their employees’ Leadership in Energy and Environmental Design (LEED) certifications.

- Business Acquisitions – Changing demographics and the retirement of professional service firm owners create an opportunity for business acquisition and expansion.

With SBA 7(a) financing, engineering companies can continue to grow alongside the trending demands of today’s marketplace.

Volume Trends: In FY2018, engineering firms obtained more than $143 million through the SBA 7(a) Loan Program, making this the year with highest dollar volume authorized to engineering firms over the last decade.

Key Statistics & Trends

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

Business Loans for Lawyers: Common Ways Attorneys Use SBA Loans

Offices of Lawyers (NAICS Code: 541110) ranked #18 in our latest research on the top 40 industries for SBA financing over the last decade. During this period, the number of business loans for lawyers reached 6,168 SBA 7(a) loans totaling roughly $1.25 billion. Attorneys find the 7(a) Program to be one of the most attractive options for financing because of the flexibility surrounding the permissible uses of proceeds, such as continuing legal education, refinancing existing debt, and working capital to cover case expenses.

If you’re considering an SBA 7(a) loan for your law practice, you’re looking into one of the best small-business loan products on the market. If you’re able to qualify, you’ll find that SBA loans tend to be advantageous in comparison to alternative commercial loan products. Lower interest rates, longer repayment terms and manageable fees are some of the primary benefits. Keep in mind, the 7(a) Program was created for small businesses to grow and succeed long-term.

Competition for jobs within the industry is expected to increase according to the U.S. Bureau of Labor Statistics as more students graduate from law school each year than there are positions available. Rather than pursuing alternative careers, many graduates may look to start their own practice, which will require start-up capital that can be obtained via SBA loans.

Common Ways Lawyers Use SBA Business Loans

Regardless of experience, the challenges of running your own legal practice can be substantial and it’s critical to understand the anticipated expenses. Below are a few examples of ways SBA loan funds can be used to help fund your growth.

- Maintaining Reputation – Firms are expected to have tastefully decorated offices and knowledgeable and licensed staff members. They need to maintain various association memberships to give the impression of credibility and professionalism to their clients, all of which can be costly.

- Marketing Campaigns – Word of mouth is excellent advertising for a law firm, but more and more, firms are looking for better ways to land additional clients and attract the best recruits. Digital advertising, T.V., and radio are some of the most common forms of marketing campaigns for attorneys.

- Specific Cases – It is becoming more common for established attorneys to seek financing for complex litigation work tied to an upcoming case they expect to win. These loans can typically be secured by a future verdict or settlement.

- Business Acquisitions – Changing demographics and the retirement of professional service firm owners create an opportunity for business acquisition and expansion.

Understanding which of these needs best fit your practice can help increase the likelihood of being approved for an SBA 7(a) loan.

Loan Size: The average loan size for law firms is much lower than national average. In FY2019, the average loan size for attorneys was $270,145 versus the national average of $450,212.

Key Statistics & Trends

Utilizing the SBA 7(a) Loan Program is one of the most popular ways for law firms to access capital. Maintaining a high level of credibility and professionalism, running marketing campaigns, and being able to accept large scale litigation work will require many legal practices to seek financing. Business loans for lawyers could have a considerable impact when starting your own practice or trying to buy an existing practice.

Ready to get started with your SBA loan application? Complete the form below to check your eligibility. A banker from Capital Bank will contact you to discuss your law firm financing options.

Apply for an SBA Loan for Your Law Firm

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.