A USDA loan could be the key to financing assisted living facilities with business-friendly terms and potential for maximizing growth for the industry.

Market projections indicate that demand in the field is growing at a disproportionate rate to the number of operational facilities. In the United States, the 2022 assisted living facility market was valued at $91.8 billion, representing just under 1 million licensed beds. There are currently 70 million Baby Boomers, a large margin of which would not have access to a facility should they need it. The industry’s value is only expected to grow at a compound annual growth rate (CAGR) of 5.53% from 2023 to 2030. Access to financing will be a factor to support the expected growth.

Key Background: Understanding USDA Loans for Assisted Living Facilities

The USDA Business and Industry (B&I) loan is our most frequently recommended loan for assisted living facility construction because of the unique terms and benefits of the loan.

- Extended Repayment Terms: Dispersing your monthly payments over a longer repayment term can facilitate healthier cash flow and more power for continued growth. Your USDA B&I loan term will depend on how you choose to use the funds, and in some cases your available collateral, with a maximum of 30 years for real estate purchases.

- Large Loan Sizes: The USDA authorizes loans of up to $25 million for eligible businesses and projects under the USDA B&I loan program.

- Rural Economy Benefits: The USDA guaranteed loan programs were created to enrich rural economies through indirect support of entrepreneurs in the area. Their mission-driven loan program makes it possible for entrepreneurs to leverage loan benefits that are comparable to the best financing terms on the market.

- Not Your Only Option: If your project is eligible for a USDA B&I loan, it’s typically the mostaffordable capital on the market for projects in areas defined as rural with 50,000 inhabitants or less. However, you may also qualify for other forms of government guaranteed financing with similar beneficial terms. A specialized lender can help you determine the most efficient way to finance your assisted living facility based on your financials and long-term goals.

Read More About How the USDA B&I Loan Program Works >

How to Leverage a USDA B&I Loan for Assisted Living Facilities

A key benefit of the USDA B&I loan program is its flexible use of proceeds, meaning that entrepreneurs have liberty to choose how they use their funds. This gives entrepreneurs the power to leverage the USDA loan in multiple ways. The following are four popular ways assisted living facility owners utilize USDA B&I loans to build, grow, and buy facilities.

1. Assisted Living Facility Construction

The USDA B&I loan could help developers finance the construction of in-demand assisted living facilities with long term, affordable capital because of the loan’s extended term for real estate. Developers of large-scale construction projects like assisted living facilities can lock in up to a 30-year term (sometimes higher) through the B&I program. This is a highly competitive benefit of the loan program. The extended loan term disperses payments over a longer period to conserve cash flow and support continued growth over time.

2. Debt Refinance for Existing Facilities

The 2020 OneRD initiative made refinancing with USDA B&I loans simpler, and made it possible to refinance up to 100% of existing loans with another lending institution through the B&I loan’s competitive extended terms If the existing debt is owed to the lender applying for the loan guarantee, then the refinancing amount owed cannot exceed 50% of the total loan request.

It may be a good option for businesses that need to improve cash flow currently restricted by debt and is particularly useful for qualified assisted living facilities that need refinancing over a longer term than their current debt allows.

3. Working Capital to Grow an Assisted Living Facility

How would you grow your facility if you had access to capital? Would you hire more staff, invest in a new website or software, or renovate? Maybe your facility needs more medical equipment, or updated technology.

Using a USDA B&I loan to access affordable working capital could put the resources in hand to make the most of upcoming opportunities for growth. Once the working capital portion of your financing package is funded, you’re at liberty to use the cash in the ways you need to grow your facility.

4. Buying an Assisted Living Facility

The USDA loan can also be used to buy an assisted living facility for sale. Using a USDA B&I loan to acquire a facility can be business-friendly way to finance acquisitions, since the extended loan term and competitive rates can help you conserve cash flow throughout the loan term.

It’s a good idea to have the business you’d like to purchase in mind before engaging a lender for a USDA loan. This helps your lender put together a more efficient and accurate financing package based on the actual business you’d like to buy.

Eligibility for USDA B&I Loan for Assisted Living Facilities

If your project qualifies for a USDA B&I loan, it’s a good option to consider. The USDA B&I loan is typically recommended by our bank as one of the best options on the market for affordable assisted living facility financing. There are three big criteria your business needs to meet to qualify for the USDA B&I program:

1. The Project Is In a Rural Area.

The USDA B&I loan program is dedicated to supporting rural industry growth and job creation. To qualify, your assisted living facility needs to be in a rural community, typically defined as an area of less than 50,000 people.

Not sure if you qualify? Check your location’s category using this rural eligibility tool on the USDA’s website.

2. The Funds Are Used for an Eligible Purpose.

The loan proceeds must be used towards business activities that support the start, growth, or construction of your assisted living facility. Most often we see the USDA loan used to construct an assisted living facility and support initiatives like hiring additional employees and modernizing the facility.

3. The Business Meets Minimum Collateral Requirements.

The USDA requires that a business fully collateralize their loan amount. That is typically satisfied by real estate and/or heavy equipment. It’s this collateral requirement that makes the USDA B&I loan such a good option for assisted living facility construction or acquisition if the seller owns the real estate. The building and real estate associated with assisted living facility projects could very well satisfy collateral requirements that can otherwise be hard to meet in other industries.

Discussing Your USDA Loan Options for Assisted Living Facility Loan

The first step towards financing at Capital Bank is pre-qualifying. After you apply online, you’ll have an initial meeting with a member of the lending team to review the USDA B&I program and other options that may fit your financing need.

After an initial conversation, your lender may ask for some more financial specifics to guide your path forward. It’s a good idea to have your business plan, financials, and business tax returns up to date and accessible for these early stages of the USDA financing process.

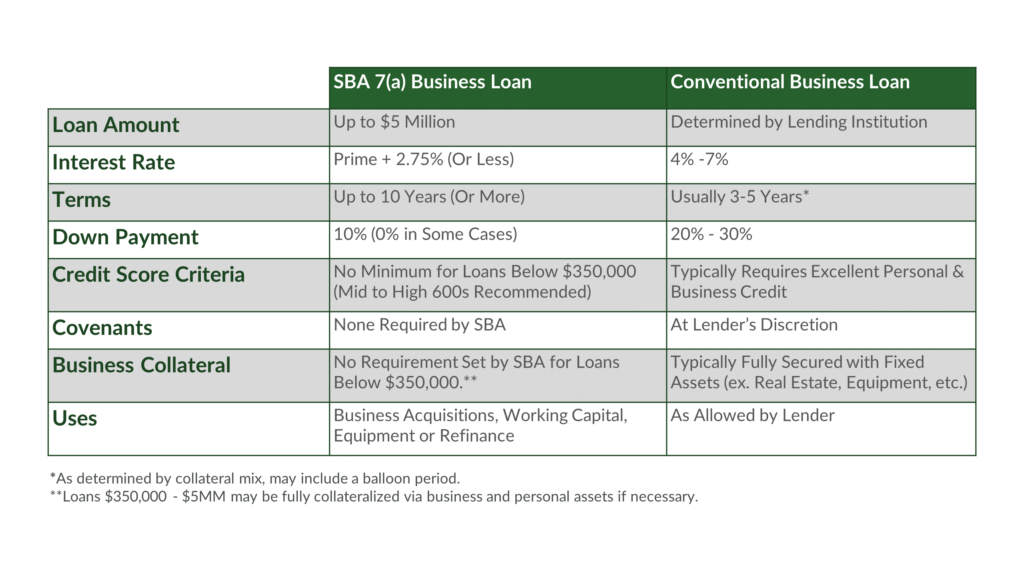

If your project is not in a rural location, or if the program isn’t the right financial fit, you could still qualify for government guaranteed financing for assisted living facilities through a different agency, namely, the Small Business Administration. The SBA 7(a) loan is equipped with a variety of similar benefits as the USDA B&I loan and can sometimes be more cost effective for loans between $100,000 – $3,000,000.

Learn more about the SBA 7(a) loan program here. >

Since no two financing scenarios are perfectly alike, it is always recommended that you speak with a lender well versed in SBA and USDA business loan programs. A specialized lending team can walk you through your options to help select the program that makes the most sense for you and your business goals.

Ready to Discuss Your

Assisted Living Facility Financing Options?

Complete the form below to pre-qualify for USDA B&I financing at Capital Bank. You’ll hear from our team shortly to discuss your best options for financing your goals.

About Capital Bank | Capital Bank is proud to serve small business owners and entrepreneurs, helping them access affordable capital and financial services when they need it most. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. We’re guided by trust, respect, and honesty, and we’re driven by “what’s next”. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being. We don’t just think outside the box, we think outside of the bank, so you can feel unquestionably confident banking with us.

Capital Bank is chartered in North Riverside, Illinois, and retains its operations in Raleigh, North Carolina.