DISCLAIMER: When you click Accept you will be leaving the Capital Bank (“the Bank”) website and are going to a website that is not operated by the Bank. We are not responsible for the content or availability of linked sites.

ABOUT THIRD PARTY LINKS ON OUR SITE

The Bank offers links to other third party websites that may be of interest to our website visitors. The links provided in our website are provided solely for your convenience and may assist you in locating other useful information on the Internet. When you click on these links you will leave the Bank’s website and will be redirected to another site. These sites are not under control of the Bank. The Bank is not responsible for the content of linked third party websites. We are not an agent for these third parties nor do we endorse or guarantee their products. We make no representation or warranty regarding the accuracy of the information contained in the linked sites. We suggest that you always verify the information obtained from linked website before acting upon this information. Also, please be aware that the security and privacy policies on these sites may be different than the bank’s policies, so please read third party privacy and security policies closely. If you have any questions or concerns about the products and services offered on linked third party websites, please contact the third-party directly.

The USDA REAP program is an excellent resource for businesses that need funding to improve or jumpstart their energy related project. REAP stands for the Rural Energy for America Program, and helps support financing needs for the purposes of purchasing or constructing renewable energy systems or making energy efficiency upgrades to a business’ operations.

Starting a renewable energy plant or investing in other energy-efficient technologies can be very capital intensive, creating a hurdle for small businesses to enter the space. USDA REAP loans offer businesses flexible terms, longer amortization, and other unique benefits that many companies cannot find in a conventional loan. These loans can help eligible small businesses grow and succeed, and the flexibility surrounding loan amounts and terms makes them more accessible.

Not all businesses are the right fit for a USDA REAP loan. The program has strict eligibility requirements that applicants should be aware of during the initial search for financing. Let’s take a look at USDA REAP eligibility and how to get started with the application process.

What Are The Eligibility Criteria For A USDA REAP Loan?

When determining if your business is eligible for a USDA REAP loan, there are three categories of eligibility that must be considered. These categories are the type of business, the type of project the funds will be used for and, lastly, how those funds will be used to benefit the business or project. To be eligible for a REAP loan, a business must be eligible in all three categories.

1. Eligible Business Types

Agricultural Producers

The first type of eligible business is an agricultural producer. To be defined as an agricultural producer, a business must have 50% or more of its gross income be attributed directly to agricultural operations for the 5 most recent years. If the business hasn’t been in operation for more than 5 years, then the gross income breakdown for the entire lifetime of the business will be considered. A business that is defined as an agricultural producer can be located anywhere in the United States.

Rural Small Businesses

The second type of eligible business is defined as a “rural small business”. Therefore, to meet the criteria, the business must be located in a rural region and considered a small business by the USDA.

First, let’s discuss how “rural” is defined by the USDA. To fit this criteria, the project that you are using the funds for must be located in a rural region. This is typically a town or rural area with less than 50,000 people. To be sure your business’ project fits the “rural” criteria, the USDA offers an online tool to check rural eligibility. The business itself can be located anywhere in the United States, but the project that the funds will be used for must be located in a rural location, as defined by the USDA.

Next, the business itself must meet the criteria of being a “small business”. The USDA uses the Small Business Administration’s (SBA) Small Business Size Standards to determine this eligibility. The SBA offers an online tool where you can check to see if you meet their Small Business Size Standards. Click here to access the SBA’s “Size Standards Tool”.

2. Eligible Project Types

Once it is determined that your type of business is eligible to receive a REAP loan, you must also determine if the project you are going to use the funds for is REAP eligible as well. Below are the two types of projects that fit into REAP eligibility:

The first type of eligible project is a renewable energy system. This can be the purchasing, construction, or installation of a renewable energy system. The USDA defines a renewable energy system as a system that provides energy from any of the following renewable resources:

Solar

Wind

Renewable Biomass

Ocean

Geothermal

Small hydro-electric

The second type of project is an effort to improve the energy efficiency of a business’ facility or building. This could include things such as insulation improvements, lighting, doors, windows, or the replacement of energy-inefficient equipment.

3. Eligible Use of Proceeds

The third piece of eligibility criteria is to determine how the proceeds of the loan will be used. Below we detail eligible ways to use of proceeds under the REAP guidelines:

Purchase or installation of a new or refurbished renewable energy system

Energy efficiency improvements that have been identified in an energy assessment or audit

Professional service fees for consultants, contractors or other third parties related to the project

Land acquisition related to the project

Working capital to assist with the completion of the project

Energy audit and assessments

It is always recommended that you speak with a lender experienced in USDA REAP lending, as they will be able to identify whether or not your plans on how to use the loan funds will qualify under the REAP guidelines.

If you’re an eligible business, a USDA REAP loan can give you the capital you need to start your renewable energy project or make improvements to your business equipment. Working with a lender experienced in USDA REAP lending, like Capital Bank, can simplify the application process and help you get the funds that you need to move forward. If you are interested in getting a REAP loan for your energy project, use the contact form below to speak to an expert who can help guide you through the process.

About Capital Bank

During each of the previous three fiscal years, Capital Bank has ranked as a top 5 USDA B&I and REAP lender in the country by total dollar volume, authorizing nearly $400 million in financing collectively during this period. Click the link below to learn more or get started with your USDA REAP financing.

As I listen to our business clients talk about how the pandemic has affected their companies, it’s like a hurricane without the wind, a 9.0 earthquake without the shaking, or a wildfire without the flames. Even though businesses haven’t been visibly demolished, many have been eviscerated. The building may be standing but it was quickly evacuated and its tenants displaced. Companies’ revenues were wiped out, slashed from millions to zero in some cases. Financial losses were huge, but COVID also exacted devastating personal losses, taking lives and livelihoods, leaving intense suffering in its wake.

What I hear in business owners’ voices is real trauma, profound loss, plus confusion about what to do next. Most people aren’t defining this struggle as Post Traumatic Stress Disorder (PTSD). But how is the pandemic any different from surviving a natural disaster or life-changing trauma? Owners are experiencing the same symptoms, intense fear, shock, anger, helplessness, horror and even guilt.

The emotional toll of what we’ve all been through during COVID-19 can’t be quantified, but it also can’t be ignored. Anyone suffering from trauma will recover faster if they get outside help. The most important thing to understand is you are not alone.

Planning Your Next Phase of Recovery

Many businesses got a lifeline through the U.S. Small Business Administration’s (SBA) Paycheck Protection Program (PPP). But that’s like being provided a FEMA trailer after a natural disaster. It offers a temporary safe haven but doesn’t help you rebuild.

In order to rebuild, your company needs money, but your balance sheet is likely in tatters after this hellacious year, which means getting a loan could be challenging.

SBA No-fee 7(a) Loan

That’s why borrowing through one of the SBA’s loan programs is a great opportunity. The SBA exists to help businesses both during periods of prosperity and times of crisis. One of the ways they do that is by offering loans that banks typically would not be willing or able to provide on their own.

If you’re wrestling with how to rebuild or expand your business post-COVID, here’s a great opportunity to consider: an SBA program called a 7(a) loan. The SBA usually charges fees with the 7(a) loan. Thanks to economic-aid legislation signed into law last year, however, the SBA is waiving fees on 7(a) loans up to $5 million. It’s the first time we’ve seen this in a decade, and it’s all part of a massive federal effort to help businesses recover from the ravages of the pandemic.

The SBA originally intended its 7(a) program to provide financial help to small businesses in particular circumstances, such as when a business needs short- and long-term working capital; needs to purchase furniture, fixtures, and supplies; seeks to refinance current business debt; and/or when real estate is part of a business purchase. But the pandemic has created historic, world-war-era hardships that require an enormous government response — including helping COVID-devastated businesses get back on their feet.

As part of that federal response, the SBA’s 7(a) loan program has been temporarily modified. The economic-relief law increased the 7(a) loan guarantee to 90% and allowed for reduced or no fees for the borrower and the lender. It also temporarily increased the 7(a) express loan limit and loan guarantee, so businesses would have access to needed working capital. And it extended the Small Business Debt Relief program, Section 1112 of the CARES Act, to defer principal and interest payments on new and existing 7(a) loans for eligible entities.

That’s the good news. The hard part is: You can’t just walk up to a window at SBA headquarters and get one of these loans. The SBA works through banks to loan out its money. And not all banks are equal in their knowledge of and experience with the ins and outs of that process. So, you want to be careful about which bank you choose to help you seek an SBA loan.

Pick the Right Partner

There are smart, and not-so-smart, strategies to consider when pursuing SBA financing. We specialize in the smart ones. In fact, we’ve got a team devoted to helping you figure out the best fit and approach for you and your business. We also advise you on the right amount to apply for.

Applying used to be a slow-motion pain in the neck, requiring loads of documentation that took forever to get approved. But Capital Bank, N.A., has transformed that experience. Our process saves you time, in part because we have a thorough understanding of eligibility requirements. The SBA’s eligibility factors are complicated, which is why working with one of our 7(a) loan experts is so important.

Rebuilding your business’s future is daunting. And it takes more than money. It takes understanding how to best use that money, before you even apply for a loan. That’s why you don’t want to just go with a bank that can do it — you want to partner with a bank that can do it well. You need a bank that’s willing to tell you what you need, not simply what you want to hear.

Most of all, you need a bank that has your back. Personally — after all the suffering, the loss, and the confusion you’ve had to face — I believe you deserve it.

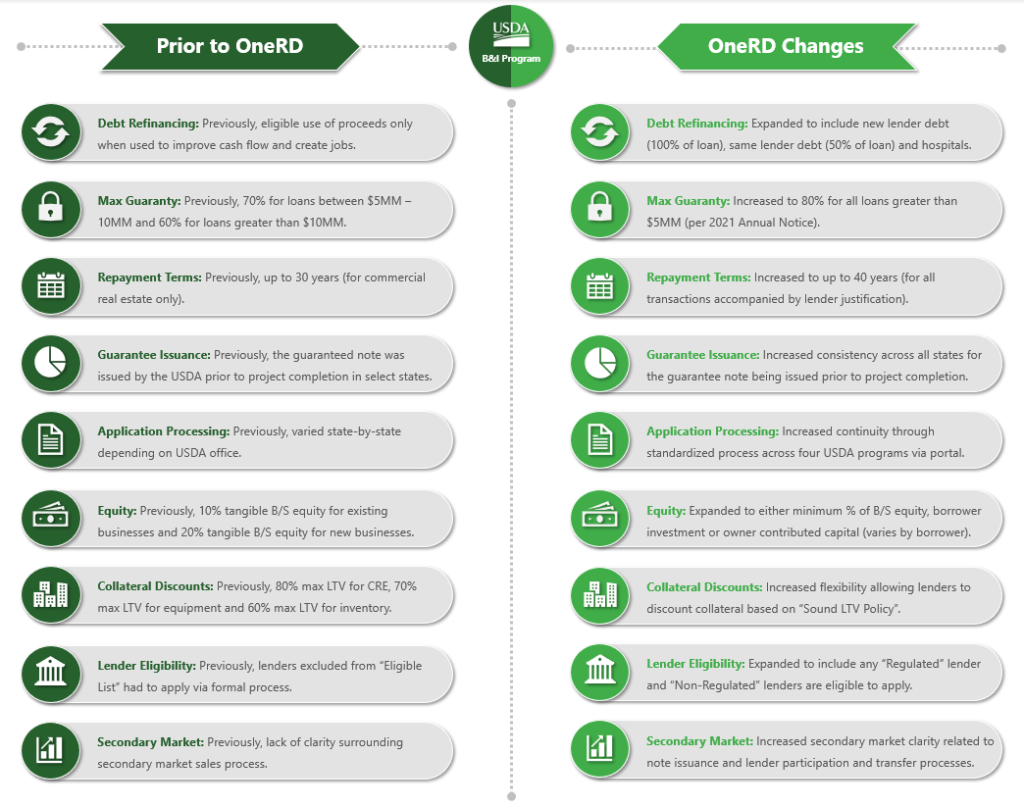

On October 1, 2020, the USDA implemented a unified platform for all of its rural development guaranteed loan programs known as the One Rural Development (OneRD) Guarantee Loan Initiative. Under OneRD, the USDA removed regulatory barriers to make it easier for private lenders to use loan programs to invest in rural businesses and economic development efforts by eliminating duplicative processes and launching standardized requirements across the following four USDA loan programs:

Major policy changes include automatic approval to lenders in good standing to participate, streamlined application processing, common applications, consistent population limits, lender-driven processes with commonly used lending practices, expansion of refinancing abilities and issuance of loan notes prior to projects being completed. Not only do consolidated rules and regulations provide increased continuity, but these updates also create new benefits for specific programs, including the USDA B&I Loan Program – the most widely used and diverse program of the four. This article highlights specific advantages for USDA B&I loan borrowers as a result of the OneRD initiative.

1. Expanded Base of Eligible Lenders

Previous regulations listed “Eligible Lenders”. If a lender was not specifically listed, they were required to undergo a formal review and approval process. OneRD now defines “Regulated Lending Entities” and “Non-Regulated Entities”. Through a single lender application, USDA provides automatic approval to “Regulated Lending Entities” in good standing that are supervised or created by State or Federal regulatory agencies to participate in all four programs. In addition, “Non-Regulated Entities” are eligible to seek approval to participate which remains valid for up to five years. This expands the base of eligible lenders and in-turn allows borrowers to choose from a larger group of financial institutions that to are eligible to participate in the B&I Program.

2. More Lenient Collateral Discount Requirements

Under previous constraints, maximum Loan-to-Value (LTV) requirements were established based on the type of collateral through the B&I Program (80% max LTV for CRE, 70% max LTV for equipment and 60% LTV for inventory). Under OneRD, collateral must have documented value sufficient to protect the interest of the lender and the Agency. Lenders are required to discount collateral consistent with sound LTV policies and discounted values must be at least equal to the loan amount. Although the lender must provide satisfactory justification of the discounts, borrowers now have the flexibility to work under the direct policies of the lender as opposed to guidelines set forth by the USDA.

3. Expanded Options for Equity Requirements

The OneRD rule removes the concept of “Tangible Balance Sheet Equity” requirements for borrowers through the B&I Program. This term had not existed anywhere else in the lexicon of financial regulations and was not recognized by the accounting profession in the context of GAAP accounting. This regulation was replaced with the requirement to have sufficient capital or equity to mitigate the on-going financial and operational risks of the business. There are now several ways for both new businesses and existing businesses to meet the B&I equity requirement, which must be met at the time of closing.

4. Additional Debt Refinancing Capabilities

OneRD states that if existing debt is owed to a lender who is not the lender applying for the loan guarantee, then the request for a loan guarantee can be for 100% of the loan(s) being refinanced. If the existing debt is owed to the lender applying for the loan guarantee, then the refinancing amount owed cannot exceed 50% of the total loan request. In addition, refinancing of rural hospital debt is a new provision to help preserve access to health services. Previous guidance simply stated that refinancing under the USDA B&I Program could be accomplished if the proceeds where being used to improve cash flow and create jobs in rural areas, which often times made it difficult for borrowers to pursue refinancing opportunities through the Program.

5. Increased Maximum Guaranty

To improve transparency and processing efficiencies, USDA now provides a standard guarantee percentage through an Annual Notice released for each program at the onset of the fiscal year. For the B&I Annual Notice for 2021, the USDA has set a standard guaranteed percentage of 80% for all loans. Previously, the guarantee percentage was tiered based on the loan amount (80% for loans under $5MM, 70% for loans ranging from $5MM – $10MM and 60% for loans in excess of $10MM). When considering transactions in excess of $10MM, a 20% increase in the guaranteed amount substantially mitigates risk for the lender and enhances the institution’s incentive for Program participation. These changes will ensure increased access to the Program among borrowers.

6. Consistent Early Loan Note Guarantee Issuance

Issuing the Loan Note Guarantee (LNG) prior to construction projects being finished was in fact already an option under the USDA B&I Program before OneRD. However, the concept of doing so was inconsistent state-by-state. With OneRD, all four programs will make this option available regardless of where the project is located, giving more borrowers peace of mind earlier in the process that financing will ultimately be secured. That said, there are risks to the Agency when issuing the LNG prior to project completion which means there are additional requirements, such as the borrower paying a 0.5% fee in addition to the one-time guarantee fee upon requesting an early LNG.

7. Extended Payment Terms

Each USDA program used to have separate loan amortization limits. In some cases, programs provided specific limits based on the type of collateral. For example, the maximum term for B&I loans would allow for repayment terms of up 30 years for commercial real estate transactions only. Through OneRD, lenders establish and justify the guaranteed loan term on a case-by-case basis which is subject to review of the Agency. The USDA’s parameters allow for a maximum 40-year proposed term limit. Longer maturities result in drastically lower monthly payments and conservation of cash flow, creating an opportunity for borrowers to grow their business faster assuming extended terms are justified and approved.

8. Streamlined Application Processing

The customer experience through the USDA B&I Program prior to the rollout of OneRD was inconsistent and choppy. Depending on which state office was handling the transaction, Agency point-of-contacts, systems and timelines varied. As part of centralizing standards across these four USDA programs, the application intake process is now streamlined and utilizes consistent application forms. Through one portal and one point-of-contact with the USDA, lenders and borrowers both have greater transparency into the status of every application. As a result, the Agency targets a 30-day window from filing to Conditional Commitment and 48 hours for issuing the guarantee when conditions are met.

9. Improved Secondary Market Sale Process

Under previous guidance, the secondary market sales process did not include sufficient documentation requirements of secondary market intent upon the loan guarantee being issued. In addition, loan participation and lender transfer processes were ambiguous. OneRD requires lenders to be clear with their intent to sell the loan and sets standards for the amount that must be retained by the originating lender (minimum of 7.5% of the total loan amount). Clarity surrounding these processes will encourage lenders to participate more frequently in the program without the burden of trying to manage a disjointed process, therefore resulting in increased access to the Program for borrowers.

As a result of the USDA consolidating eligibility requirements, credit review guidelines and loan processing channels across its four main lending programs, lenders and borrowers alike now have greater access to USDA financing options. Specifically, consistent standards and rules should allow more rural businesses to take advantage of the many benefits offered through the USDA B&I Program. Extended terms, faster turn-times and increased flexibility through the USDA’s OneRD updates reflect the Agency’s mission to provide a better overall experience for borrowers.

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

During each of the previous three fiscal years, Capital Bank has ranked as a top 5 USDA B&I and REAP lender in the country by total dollar volume, authorizing nearly $400 million in financing collectively during this period.

Interest on Lawyer Trust Accounts (IOLTAs) have strict rules. Lawyers are not allowed to earn interest on its clients’ funds by law so the interest generated on these accounts is automatically funneled to the respective state IOLTA board which will apply those funds to help a charity or educational program, improve the administration of justice, and pay for legal aid for low-income residents. To make managing IOLTAs even more complex, the rules vary state-by-state. Plus, all IOLTA accounts (regardless of state) must conform to the principles of double-entry accounting. However, with the right diligence, you can avoid potential problems, financial losses and disciplinary action.

If you have a good understanding of IOLTA account rules, keep careful records, and ensure that a CPA and reputable bank are overseeing your business and client trust accounts, you can avoid the mistakes that many lawyers make.

Here are five of the most common.

1. Commingling Funds

IOLTA accounts need to be reserved for the client’s account only. You can’t, for example, pay for your firm’s operating expenses directly out of an IOLTA account. You need to move those funds into a business account first. This rule is upheld for each IOLTA board for every state.

2. Charging Payment Fees

The passing on of bank service charges for wire transfers, paper statements and re-ordering checks, as well as fees pertaining to other clients’ cases, is another other common and inadvertent mistake lawyers can make when managing trust accounts.

3. Borrowing Money

Sometimes attorneys use trust account funds before they have a right to do so. They might take trust account money before it’s earned because they’re having cash flow problems. There’s no legitimate way to borrow from a trust account, but some attorneys try. It’s often intentional and it’s the quickest way to find yourself in hot water.

4. Poor Record Keeping

Attorneys are required by their bar associations to keep records showing how much money each client has in trust at any given time, but they don’t always keep true and accurate records. Deposits and disbursements must be clearly tracked in a way that makes it easy to determine each client’s trust account balance and transaction history.

5. Not Getting Help

This last and potentially most costly mistake is related less to IOLTA account rules, and more to humans being humans. When some attorneys realize they’ve made a mistake, instead of seeking out professional help, they try fixing it themselves. Which can often create a whole new set of problems. Be smart, get help.

Now you know some of the most common IOLTA mistakes. You may even have experienced one of them yourself. With so many IOLTA account rules, mistakes are not hard to make. The good news is, there are plenty of great options to help you steer clear of these mistakes in the future.

If there’s the possibility of a mismanaged account, contact a practice management advisor in your state. These consultants usually have experience dealing with IOLTA account rules, and most states don’t require them to report ethics violations to the bar.

If the account was setup incorrectly and you’re just starting out in early growth stages, talk to a CPA or bank with experience dealing with IOLTAs.

If you simply don’t have the time to worry about managing these accounts, consider hiring a bookkeeper with law firm expertise.

If you may have accidentally charged your client bank fees, speak with a reputable bank about ways they can assist in setting fees to be debited directly from operating accounts instead.

As you work within the IOLTA account rules, the last thing you want to do is to commit a mistake that could turn into more time worrying about the accounts, instead of taking the valuable time you’d like to spend growing your business.

Mismanaging these accounts is actually quite common and there are plenty of great resources to help you. Start with a trusted resource like a bank that’s steeped in IOLTA knowledge, to help you set up and manage your accounts in compliance.

About Capital Bank

Capital Bank is an Illinois state-chartered bank headquartered in North Riverside which provides traditional banking services to its personal and business clients within the greater Chicagoland area. Primary deposit products are checking, savings, and certificate of deposit accounts, and primary lending products are government guaranteed lending, residential mortgage, commercial and installment loans.

Whether solutions come from surprisingly innovative tools, or trusted products you’re familiar with, our single-focused purpose is to understand your goals and challenges so we can make you can feel unquestionably confident banking with us.

Anyone that has touched the Paycheck Protection Program (PPP) in some way, shape or form – business owners, bankers, accountants or otherwise – can likely agree that the only certainty has been uncertainty these past eight months.

On March 27, 2020, the President signed into law the Coronavirus Aid, Relief and Economic Security Act (also known as the CARES Act). Shortly thereafter, the $660 billion program was born in a flash as the SBA and Treasury scrambled to set program guidelines that would allow lenders to get funds into the hands of millions of business owners in dire need of a lifeline in the midst of a surging pandemic. Rules were established in less than one week and the issuance of subsequent guidance along the way, such Interim Final Rule updates and FAQ documents, have often raised more questions than answers. This has left many businesses turning to CPAs for clarity to help navigate the confusion.

PPP Forgiveness Process

On August 10, 2020, the SBA opened its doors to start accepting forgiveness applications from PPP borrowers. With more than 5.2 million PPP borrowers starting to work through the process to receiving full forgiveness, CPAs are under pressure to help manage and navigate the PPP forgiveness process. To help CPAs clearly articulate the situation to business owners, let’s first take a look at what CPAs need to know about five different areas of the PPP forgiveness application process.

1. Forgiveness Application Forms

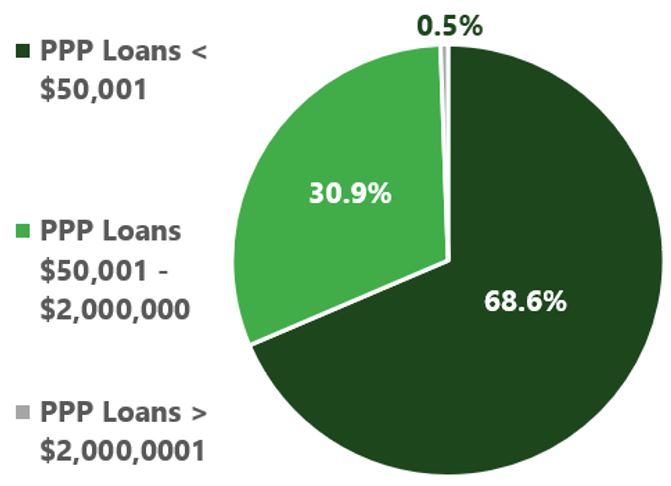

Borrowers must apply for forgiveness through the lender that disbursed its PPP loan, not directly with the SBA. The first step is to complete one of the three forgiveness application forms, dependent on the borrower’s PPP loan amount and circumstances. Per SBA data released on August 8, 2020, the vast majority of PPP borrowers are eligible to use SBA Form 3508S, the most simplified version of the three options, which include:

SBA Form 3508S – Borrowers that received $50,000 or less (68.6% of all PPP borrowers).

SBA Form 3508EZ – Borrowers that received $50,001 or more and did not reduce employee levels, wages and hours.

SBA Form 3508 – Borrowers that do not qualify to use Form 3508S or Form 3508EZ.

2. Application Submission Dates

As long as a borrower submits its loan forgiveness application within 10 months of the completion of the “Covered Period” – defined as the period a borrower is eligible to use its PPP proceeds – the borrower is not required to make any loan payments until the final forgiveness amount is remitted to the lender by the SBA. The PPP Flexibility Act (PPPFA) signed into law June 5, 2020, extended the Covered Period from eight (8) weeks to 24 weeks. For loans funded prior to June 5, 2020, borrowers can choose to keep the original eight (8) week Covered Period or move to the 24-week period. If the loan was funded after June 5, 2020, the borrower must adhere to a 24-week Covered Period.

3. Lender Review & Decisioning

Upon receiving a PPP forgiveness application, the lender has 60 days to issue a decision regarding forgiveness of the PPP loan to the SBA. During those 60 days, the lender must confirm receipt of the borrower’s complete application, certifications, supporting documentation and calculations that at least 60% of the loan forgiveness amount requested is attributable to eligible payroll costs with the remaining 40% attributable to eligible non-payroll costs. It is the borrower’s responsibility to provide accurate calculations, but lenders are expected to perform a “good-faith” review. If the lender identifies calculation errors or a material lack of substantiating documentation, the lender should work with the borrower to correct any issues. Once the lender makes a PPP loan forgiveness decision, the decision is then issued to the SBA.

4. SBA Review & Decisioning

After the lender issues its PPP loan forgiveness decision to the SBA, the SBA has 90 days to validate or deny the lender’s decision and remit the appropriate forgiveness amount, including accrued interest, to the lender. Although nothing is set in stone, borrowers that received a PPP loan in excess of $2 million will likely be required to complete and return a PPP loan Necessity Questionnaire (either SBA Form 3509 for for-profit businesses or SBA Form 3510 for non-profit businesses, although both forms are still unofficial) within 10 days of receipt from the lender. While the microscope may lean more heavily on this demographic of borrowers, all PPP borrowers may be subject, at any time, to the SBA’s review of borrower eligibility, unauthorized use of funds and loan forgiveness, in the SBA’s sole discretion. All borrowers and their advisers should have a general understanding of what an SBA Loan Review is and how to appeal an adverse decision from the SBA, if necessary.

5. Borrower “Right to Appeal”

If a borrower faces an adverse SBA Loan Review decision (defined below), it must respond quickly. In order to appeal the SBA Loan Review decision to the SBA Office of Hearings and Appeals (OHA), a borrower must file a petition with OHA within 30 calendar days after receiving the final decision or being notified by the lender of the final decision. Any decision that does not fall under the definition of an SBA Loan Review cannot be appealed to OHA. For example, there is no appeal option for a borrower if the lender partially approves forgiveness and the SBA remits the partial PPP loan forgiveness amount.

Moving Targets

Additional PPP guidance remains forthcoming. Borrowers and their advisers must not only understand the general process when applying for forgiveness, but also the many gray areas within guidance that can easily be misinterpreted or changed upon further direction from Washington. Here are some of these “moving targets” to consider prior to filing for forgiveness, many of which will only be applicable to specific situations for specific borrowers:

Early Borrower Submissions

While early applications are permitted, the eight (8) or 24-week Covered Period must be considered. Whether it’s eight (8) weeks or 24 weeks, borrowers may apply for forgiveness before the end of the Covered Period. However, doing so lowers the maximum eligible compensation. If a borrower exhausts its PPP funds for eligible expenses and chooses to apply for forgiveness 16 weeks after the start of the Covered Period, the period would still be 24 weeks and compensation maximums for employees would be prorated, less than the compensation maximum for employees of borrowers with a 24-week Covered Period. In this example, it becomes quite ambiguous if the borrower makes employee changes impacting compensation maximums during the Covered Period at week 22 but elected to apply for early forgiveness at week 16. The prorated compensation maximums at the time the application was submitted for forgiveness would not be accurately reflected as the law is currently written.

Blanket Forgiveness

Since the PPP forgiveness process can be tedious, even with simplified forms for certain borrowers, members of Congress have proposed legislation that would allow for a much more streamlined PPP forgiveness process. There is anticipation among lenders and borrowers alike that loans of $150,000 or less will automatically receive full forgiveness with a certification by the borrower that the money was used according to guidelines. As talks continue to press forward on this idea, there is a possibility that “blanket forgiveness” for the more than 87% of all PPP borrowers that fall in this category won’t ever be granted by Congress. For borrowers meeting this description that have yet to prepare the documentation required for PPP forgiveness submission, it might make sense to wait and see how the pending rule shakes out prior to moving forward with filing for forgiveness.

Deducting Expenses

IRS Notice 2020-32 declared that no tax deduction is allowed for an expense that is otherwise deductible if the payment of the expense results in forgiveness of a PPP loan. This argument states that allowing the deductibility of expenses paid with PPP funds would result in borrowers “double dipping”. Hundreds of organizations, including the American Institute of Certified Public Accountants (AICPA), are urging Congress to allow full deductions for PPP-related expenses given the severity of COVID’s impact on businesses across the country. There is a case to be made that Congress originally had intended PPP expenses to be deductible and lawmakers from both parties have voiced support for this position with no material action yet to be settled. Should full deductions for PPP-related expenses be allowed, eligible tax years start to get dicey for borrowers that incurred these expenses during a specific fiscal year but didn’t receive forgiveness until the following fiscal year.

Economic Injury Disaster Loan (EIDL) Advances

The EIDL Program was activated several weeks before Congress passed the CARES Act, making it the first Federal small business aid program to address the economic crisis. Different than PPP, EIDL loans were handled directly by the SBA rather than through private lenders so entrepreneurs that didn’t have deep banking-industry connections could swiftly access relief. Due to the enormous backlog of EIDL applicants, SBA offered an immediate EIDL Advance (up to a $10,000 maximum) within three days of applying for an EIDL loan, meant to serve as an interim but vital source of funds while applicants awaited a decision on their EIDL loan application. To access the EIDL Advance, recipients first had to apply for an EIDL loan but did not have to be approved to receive the EIDL Advance. However, those that were also applying for a PPP loan were asked to net the EIDL Advance that had been received out of the request for PPP funds. Whether borrowers overlooked netting out the EIDL Advance or had yet to receive EIDL Advance funds at the time the initial PPP loan application was submitted, these businesses are now having the amount of the EIDL Advance subtracted from the PPP loan forgiveness amount. This has many up in arms as guidelines originally stated the EIDL Advance did not have to be repaid. Nearly six million small businesses secured an EIDL Advance and rumors continue to float around as to whether this rule will stand.

Business Structural Changes

Countless borrowers have had to revise business structures in the face of the pandemic. Alterations to a company’s legal structure, a decrease in employee count or eliminating a business division after a borrower receives a PPP loan may impact the borrower’s ability to receive full, or partial, PPP loan forgiveness. On October 2, 2020 (almost two months after PPP forgiveness applications could start being accepted), the SBA released a Procedural Notice concerning required procedures for changes in ownership of an entity that has received PPP funds. Under the Procedural Notice, a Change of Ownership will be considered to have occurred when either: (i) at least 20% of ownership interest of a PPP borrower is sold or transferred; (ii) the PPP borrower sells or transfers at least 50% of its assets; or (iii) a PPP borrower is merged with another entity. In addition, SBA approval or funding PPP loan balances into escrow may be required in connection with a Change of Ownership transaction and purchasers may be required to assume the PPP borrower’s obligations. If the PPP loan is in place and lender consents are required, then the parties need to consider whether the Change of Ownership transaction could trigger a default under the PPP loan documents and a loss of potential forgiveness.

What Can CPAs Do Now Relative to the PPP Forgiveness Process?

Be Patient

For CPAs to effectively help business owners reach the forgiveness finish line, basic knowledge of the overall process is required, as well as an understanding of certain gray areas and potential rule changes that may impact forgiveness decisions depending on a borrower’s situation. If rule changes are still in limbo that could be significantly beneficial to a client’s forgiveness consideration, the best thing to do is to be patient.

Borrowers and their advisers must not only know the rules, but also how to use existing guidance in place to come to reasonable conclusions. This is where the best judgement scenarios from CPAs come into play.

Document Everything

This cannot be stressed enough. Not only do PPP forgiveness applications require the accompaniment of detailed supporting documentation, the SBA has the right to request retained borrower information as part of its review at any time. If a borrower does not promptly provide the information being requested, this may cause a delay in PPP forgiveness processing and decisioning. In addition, it’s a general best practice to keep a paper trail of evidence supporting conclusions that were made along the way. Not to mention, the SBA requires that a borrower maintain its PPP loan documentation for up to six (6) years after the date forgiveness is received.

Through its access to intake, documentation and closing software, Capital Bank processed hundreds of PPP loans, helping preserve and maintain thousands of jobs across America throughout the pandemic. In addition, working directly with a Lender Service Provider (LSP), which helped process more than 17,000 PPP loans on behalf of nearly 50 lenders, allowed a community bank like Capital Bank to gain access to knowledge from all angles of the PPP lending process given the high volume handled by its LSP. If you are a CPA in need of a lender’s perspective of the PPP forgiveness process, please do not hesitate to give us a call at (919) 647-9581.

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

Among the many ways technology has significantly impacted the banking industry, none may loom as large as consumer expectations. People, and businesses, are getting used to – and sometimes demanding – improvements in speed and efficiency on a regular basis. But while small business owners look for quick lending solutions, they also wonder if it will be done right.

The most important thing that hasn’t changed in banking is a bankers’ ability to help small businesses conduct transactions safely and successfully. It’s why professional, experienced, trustworthy community banking partners are as important as ever.

For small businesses looking to take advantage of technology efficiencies and still make sure they have the assurance of a community bank by their side, there’s a solution:

Work with a bank that partners with technology service providers to enjoy the benefits of both worlds.

How We Got Here

For decades, small businesses have been the lifeblood of our nation’s economy. They create two-thirds of net new jobs* and account for 44% of U.S. economic activity.** Community banks have been at the heart of small businesses’ lending solutions, fueling their growth by providing the funds to help them thrive. According to the Independent Community Bankers Association, community banks fund roughly 60% of all small business loans across the country. Small businesses and community banks have successfully grown together for a long time.

Technology has also had a significant impact on small business lending solutions, especially over the last decade. According to the SBA’s FY 2019 Agency Financial Report, technology has evolved so that entrepreneurs have greater access to markets and more capabilities to start and expand their businesses.

There are several examples of how banks and borrowers can now connect more efficiently:

Marketing Technologies – Customer Relationship Management system (Salesforce), Social Media (LinkedIn) and Automation (Pardot)

Analytical Technologies – Credit Scoring (PayNet) and Spreading Financials (Sageworks)

Operational Technologies – File Sharing (Citrix) and Electronic Signatures (DocuSign)

As FinTech (Financial Technology) has grown, we’ve seen the rapid emergence of FinTech lenders like OnDeck and Kabbage. Online marketplaces have appeared, acting as a catalyst for the small business lending community, creating new speeds and efficiencies on what sometimes seems like a daily basis. Online lending is growing and there’s no end in sight.

According to the Federal Reserve’s Small Business Credit Survey, an annual survey of small businesses, credit seekers are increasingly turning to online lenders. Over the past three years, the share of applicants that reported applying with an online lender increased from 19% in 2016 to 24% in 2017, and to 32% in 2018.

It’s easy to see the benefits FinTech lenders bring. Community banks that work best with small businesses don’t just recognize those benefits, they embrace them, because they enable banks to more effectively serve their small business clients. To get the best of both worlds, it’s important to be reminded of the difference between Fintech lenders and banks.

Marketplace lenders, such as OnDeck, Kabbage, and SoFi, can serve credit needs in markets where financial institutions would not traditionally lend, allowing small businesses to access otherwise unavailable capital. However, marketplace loans tend to carry higher interest rates than traditional bank loans. That’s one of many advantages of smaller community banks. Here are three more:

Advantage #1: Assurance – Traditional banks are supervised by the OCC and/or FDIC, which provides an additional layer of consumer protection and safety by ensuring secure and reasonable rates.

Advantage #2: Relationships – Community banks and bankers build long-term relationships through expanded financial resources, including deposits, mortgages, and credit cards. Successful small business banking is about connections, not just transactions.

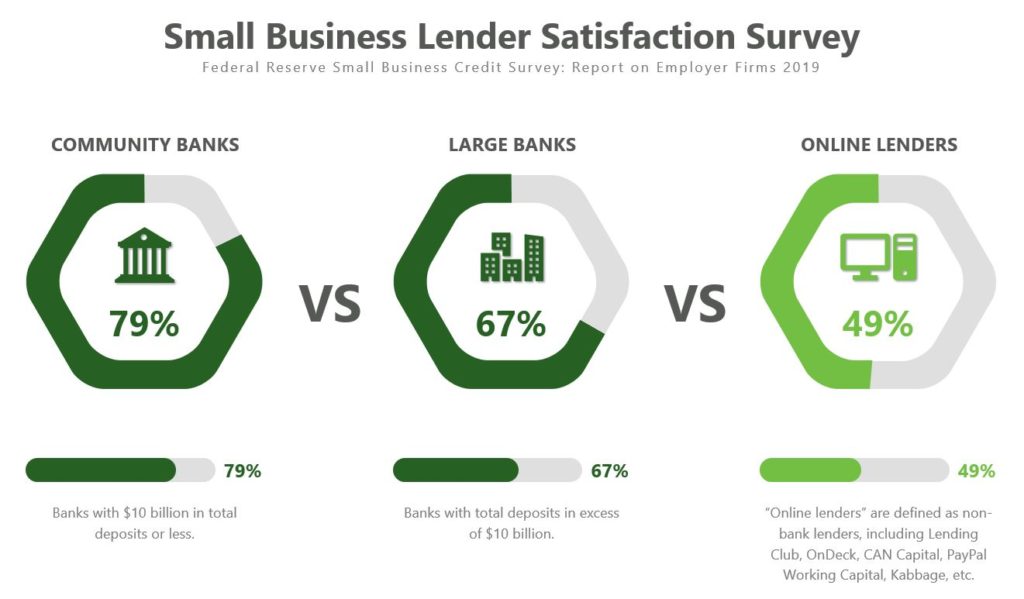

Advantage #3: Expertise – It’s hard to overestimate the value of face-to-face expertise. At a community bank, you’ll work with a dedicated banker, so you can build a rapport with a trusted source of financing and have answers to your questions at your fingertips. According to the Independent Community Bankers Association, 79% of businesses that used community banks reported satisfaction with their overall experience, compared with 67% for large banks and just 49% for online lenders.

When it comes to SBA loans, what’s the best way for a bank to combine their assurance and expertise with the speed and efficiency that technology brings? Well, some banks may have the budget to spend $11 billion on technology upgrades like JPMorgan did last year (according to Forbes). But at Capital Bank, we don’t have to spend big to bring big value to our customers.

We‘ve partnered with Windsor Advantage, LLC (a Loan Service Provider to community banks) to create “Accel,” an efficient and effective funding platform for small business lending solutions across the country. Accel (a division of Windsor) became a leader in the SBA FinTech space by investing in a best-in-class technology-enabled program that delivers small business clients a seamless application, pre-qualification, underwriting and closing process for SBA 7(a) loans of $350,000 or less. Combined with our lending expertise, it’s a safe, secure, and efficient way to get your SBA loan through the 7(a) Program.

Getting Your SBA Loan

In closing, here is a snapshot of Capital Bank’s small business lending platform – what it is and where to start.

The SBA “Small Loan” platform at Capital Bank provides small businesses with a fully digitized application and prescreening process, resulting in highly efficient turn-times to funding. Here are the basic facts you should know:

Loan Amount – Loans range from $10,000 to $350,000

Terms – Up to 10 years fully amortizing with no prepayment penalty

Use of Proceeds – Funds can be used for working capital, debt refinancing, equipment and business acquisitions

Capital Requirements – 100% financing available for working capital and debt refinance only.

Timelines – Secure funds in as quickly as 30 days from initial application

Collateral – Best available lien position on business assets

It’s hard not to argue that technology has made banking better. But it’s also clear that even with all of the upsides around speed and efficiency, there are still opportunities to improve how technology affects your banking experience. This is especially true when it comes to finding small business lending solutions, where it’s as important as ever to have a banking partner you can trust for safety, expertise, and meeting and beating your banking expectations. With the right technology, coupled with the right banking partner, you’ll have the best of both worlds.

About Capital Bank

At Capital Bank, our most important goal is to understand what’s important to you, what’s getting in your way, and what you hope to achieve, so we can help you get there. Since 1922, we’ve been creating long-lasting relationships with our customers based on old-fashioned values and future-thinking ideas. Whether solutions come from surprisingly innovative tools or trusted products you’re familiar with, our single-focused purpose is your financial well-being.

Capital is one of the first banks to market to fully embrace partnerships with technology service providers to better serve its customers.

About the Author: Dalton Martier has nearly 10 years of financial services experience, ranging from retirement planning, mortgages, and SBA 7(a) lending. Dalton joined Capital Bank in 2021 as a Business Development Officer focusing on underserved SBA 7(a) small loans, ($100,000 to $350,000). Dalton earned his Bachelors in International Business, Management, and Marketing from the College of Charleston. Prior to Capital Bank, Dalton was a lead Account Executive for the Nation’s largest SBA lender service provider, Windsor Advantage, LLC.To learn more, email Dalton at [email protected]or call (843) 588-7186.

“One thing I believe to the fullest is that if you think and achieve as a team, the individual accolades will take care of themselves. Talent wins games, but teamwork and intelligence win championships.” That quote from Michael Jordan has been on my mind lately as I reflect on lessons we’re all learning during the COVID-19 crisis. Jordan’s observation about teams certainly applies to our recent experiences at Capital Bank. Responding to this crisis has been a powerful reminder that a community of committed people can achieve incredible things when they come together around a common set of values.

We’ve been serving the greater DMV community since 1999, and we’ve seen our region’s economy grow to reflect a diverse mix of small-to-medium businesses with a variety of financial needs. The coronavirus hit these companies like a tsunami. Then, the Paycheck Protection Program hit banks like a second tidal wave, as businesses frantically sought help while they were trying to unravel PPP’s complicated application process. But in just two months, Capital Bank processed the equivalent of two years’ worth of loan applications, which helped uplift 37,000 employees from companies all around the DMV region during the crisis.

PPP required rapid action. Before the Small Business Administration (SBA) had even developed all the rules, for example, we had to dive in and figure out how to structure processes that would work for loan applicants and for us. We had to leverage our in-house technology to set up a platform that enabled business owners to upload all the SBA-required documentation. Capital Bank employees from all parts of the company were giving up their nights and weekends to help get it all done. Our entire team rose to the occasion, and I know many other business owners saw their people go above and beyond as well.

There was a lot at stake. As Greenwich Associates recently reported, “more than one in five small businesses and one in seven middle market companies indicate they are likely to switch banks” due to performance issues during the COVID-19 crisis. In fact, nearly half of the loan applicants we assisted had not been Capital Bank customers prior to the crisis. Our willingness to develop new solutions, make the process as easy as possible for applicants, and stick with our personalized approach to serving business owners, set us apart from many larger institutions.

Tailoring Solutions for Each Customer

One of the reasons we were able to pull together and move mountains was, we’re an entrepreneurial organization that specializes in serving entrepreneurs. Entrepreneurial thinking is embedded in our core values and drives our company culture. When you’re an entrepreneur, you recognize that each customer is unique, with real problems that you can help solve. A real entrepreneur isn’t focused on mass production, he’s looking at how to solve problems, one customer at a time.

That’s especially true in a service business like ours, where we’re not stamping out widgets, but rather passionately creating custom solutions for each individual customer. We know what it means to be an underdog, to put your whole business on the line in service to customers and to a core idea that your business stands for something special. Inventing a new and better way of doing business, of meeting a market need, that’s what entrepreneurs do.

Navigating Challenges with a Personal Approach

We’ve always made building a unique and personal relationship with each customer our number-one focus, but this PPP process took that to a whole new level. Small business owners and larger company CEOs who came to us for help had the weight of their employees and their families on their shoulders. You could hear the strain in their voice. They were desperately trying to save jobs, to figure out a way to stay in business for the next month, and the month after that, so families wouldn’t go hungry.

PPP was as confusing for banks as it was for the employers it was aimed at helping. Before the Small Business Administration (SBA) had even finalized its rules, we had to jump in with both feet to help employers navigate the loan application process. To say that we did what we always do — provide personalized service, communicate frequently, adapt to changing circumstances — doesn’t do justice to all of our people here at Capital Bank. I was humbled and gratified to watch how our team responded during the crisis.

Engaging Employees to Achieve the Unthinkable

Study after study in business has found that high employee engagement boosts performance. And a poll by Gallup showed that employee engagement is at a 20-year high. Gallup defined engaged employees as “those who are involved in, enthusiastic about and committed to their work and workplace.”

But all that research barely begins to describe the “engagement” our employees showed day after day to adjust their approach, in real time, as the SBA was finalizing their rules. We had to serve our customers and get them through the process, which involved some guesswork, while the process kept changing.

Our people tapped into their inner Michael Jordan. It was the famous triangle offense, where no one player dominated but all worked to move the ball where it needed to be, played out daily— not only within Capital Bank but more broadly at thousands of businesses in thousands of communities.

Not everyone masters teamwork and creating an all-for-one culture that’s focused on solving problems. But for entrepreneurs, for companies like yours and mine, engaged employees pulling in the same direction as a team make all the difference when you’re facing a big challenge and have to move mountains.

Unless you’re a service-based business that must get “up close and personal” with clients, it’s likely that your business depends almost entirely on digital tools for most of your communications and interactions.

AT&T found that 66 percent of small businesses would fail without wireless technology, while 41% of business owners have plans to increase technology spending. While technology increases efficiency and even time management and productivity there is still a need for face-to-face interaction for successful business.

The Value of One-on-One

In-person meetings can cost time and money, but it’s a small price to pay for that personal connection that’s critical to the success of any business. Consider a recent study in Harvard Business Review that found face-to-face requests are 34 times more likely to garner positive response over email. Cvent reports that 96% of small businesses surveyed said in-person meetings yield a return on investment. Inc. Magazine reports that 46% of professionals say they’ve lost a client or contract because they didn’t allow for enough face time and that 69% of people surveyed admit to browsing social media to pass the time on audio-only conference calls.

Also consider that a personal connection builds trust and allows you to read body language and facial expresses, which can reduce misunderstandings. Since approximately 93% of communication is non-verbal, meeting in person provides the full picture.

Beyond Meetings

It’s common to think “meetings” when you think “face-to-face.” But there’s a world of opportunities outside the office. Hosting your clients, donors, centers of influence and prospects at your own events can make a big impact. In fact, it provides a unique opportunity to catch-up with long-time connections and build relationships with those getting to know you and your business.

At Capital Bank, while we’re tech forward and digitally focused, we’ve also found hosting in-person symposiums with thought leaders and panels offers unique value to our clients, providing information they can use to inspire and change their day-to-day. Investing in events offers unique insight, and that sets us apart from other firms. More laid-back events have also proven to be a great way to get together with our clients in a more relaxed atmosphere, building personal relationships and getting the insight we might not have otherwise gotten in a traditional office setting.

Do your clients host dinners, networking events or galas? Show up for them. Nothing can be more valuable than supporting your clients in person. It gives you the opportunity to network, yet even more importantly, lets your client know you’re there for them and believe in them.

Engaging Employees

If a business has three or 300 employees, leaders should invest in time with their teams. At Capital Bank, for instance, while we enjoy events together throughout the year, we also have an annual in-person road show and town hall meeting. These events offer the opportunity for employees to go one-on-one time with the executive team, meet one another, hear details about the bank’s progress and have their questions and concerns heard. As I mentioned in a previous post, retaining is recruiting. You should be engaging, interacting and recruiting your own employees every day by challenging them to grow and succeed at work while supporting them in their personal lives.

Whether it’s with employees or clients, the human element can help give you the competitive edge in this age of email and text exchanges.

Previously, we talked about cash flow and the importance of bridging gaps before they happen. But do you know how to prepare if your business needs to take on debt? Perhaps you want to expand your business, or you’re pursuing other opportunities.

According to a recent report by the Federal Reserve, nearly 60% of small businesses applied for financing in 2017. Of those, 23% were denied financing1. How, then, can you help ensure you’re creditworthy and approved for the loan and amount you need, when you need it?

Have your Financials and Know Key Metrics

When seeking financing, it’s important to come prepared with up-to-date financials. A good outline would be to consider bringing the last two consecutive years of revenue data along with the last three consecutive years of tax information, expenses, assets, liabilities, inventory, , and accounts payable and receivable, among other things. The extra step is to prepare projections of your cash flow needs for the coming two years (minimally) which helps a possible banker or lender evaluate your ability to pay back your loan. Having all of these items in hand at your initial meeting can help save you time and work later on, while demonstrating your knowledge of your business – where it’s been and where it’s going.

Before your banker or lender will commit to a loan, their underwriting department will look at a few key metrics. Among other things they will review:

Earnings Before Interest, Depreciation & Amortization (E.B.I.D.A.):This is a conservative measure of cash flow and provides an idea of how much cash is available to handle the debt. This metric indicates cash-flow by measuring a company’s earnings. E.B.I.D.A. adds interest expenses, depreciation and amortization back to the net income number while taking tax expenses into consideration. To calculate, take operating profit, add the sum of any depreciation and then add the sum of any expenses due to amortization.

Debt Service Coverage Ratio (D.S.C.R.): This metric demonstrates that there’s sufficient cash to cover payments. It’s defined as historic E.B.I.D.A., less cash distributions to shareholders, divided by your total annual debt service obligations for its calculation.

Remember Commonly Forgotten Tax Information

Often business owners will come prepared for a loan meeting with tax returns, but sometimes supplemental tax information is needed down the line. If you have stake or ownership in several businesses, a lender will likely need to see your schedule K1 to assess the performance of all sources of income from the guarantor—even from businesses not involved in the transaction. Knowing your tax status is important too, be sure to have documentation that you’re current on your taxes, as well as your payroll taxes. If you, like many businesses, file for extensions on your taxes you’ll need all of your statements from the prior year. If you’re three months or more into the next year without filing, you should also be prepared with your W-2 and all interim statements.

When Business Gets Personal

Another factor a banker will consider is your personal credit. Credit can be complex, and many business owners are surprised when they learn their personal credit is looked at when securing business financing. Fact is, while nimble and creative lenders can often use compensating factors, like liquidity, additional collateral, great references, or well-established trade lines to overcome credit challenges, personal credit is still important, especially if you’re in the early stages of a business.

Business credit can also play a part. The Nav American Dream Gap Survey2 showed that 45% of small business owners didn’t know they had a business credit score and 82% didn’t know how to interpret their score.

It’s a good idea to start building business credit history as early as possible in the life of your business. Using your Employer Identification Number (EIN), establish trade lines with vendors and suppliers that report to all three bureaus: Dun and Bradstreet, Experian, and Equifax — Equifax being the most commonly run business credit profile. Keep in mind, however, your personal credit score will still come into play. So work toward building your business and a solid business credit score.

Work With a Consultative Banker or Lender

Finding a banker that’s a good fit for your business is also very important. Many larger institutions will offer standard solutions that might not fit your specific companies lending needs or only take on larger businesses. It’s important to find a banking partner that will take the time to learn about your business to best advise you on precisely what’s needed, and then help you determine whether to take on the loan that’s being asked for at face value, or if there’s a better structure or solution that the business owner may have not even thought possible.

Establish banking relationships early. If you know you’re going to need a loan in the future, do your shopping around well before you need financing. Ensuring you’re working with a banker who offers what you need will save you time researching when you’re ready.

Bottom line: preparation, a good credit score — both personal and business — and a consultative banker can help ensure you get the business loan you need, without surprises or delays.